Tax examination; upon a sectoral complaint or the determination of the tax authorities, fake or misleading documents in terms of content occur in terms of taxpayers who issue invoices.

Legal documents and books are requested primarily from taxpayers in tax inspection. This situation is notified to the taxpayers as a submission letter. If the documents are not submitted after the notification of the submission letter; There are consequences such as the refusal of the value added tax deductions subject to deduction in that period, smuggling in the sense of the VAT (tax loss penalty of 3 times about the VAT refused discount) and criminal complaints arising from not submitting books and documents within the scope of criminal law.

As a result of the tax examination, an assessment with a single tax loss penalty or an assessment with a 3 times tax penalty may occur.

The taxpayers have the right to compromise in the single-fold penalty assessment, but if the smuggling acts within the scope of the Law No. 213, article 359 are detected, a 3-fold penalty assessment occurs and the taxpayers have no right to compromise. In this case, the taxpayer is obliged to file a lawsuit within 30 days after the notice is served.

Reconciliation, which is one of the solutions of tax disputes at administrative stage. It is divided into two as pre-assessment and post-assessment settlement.

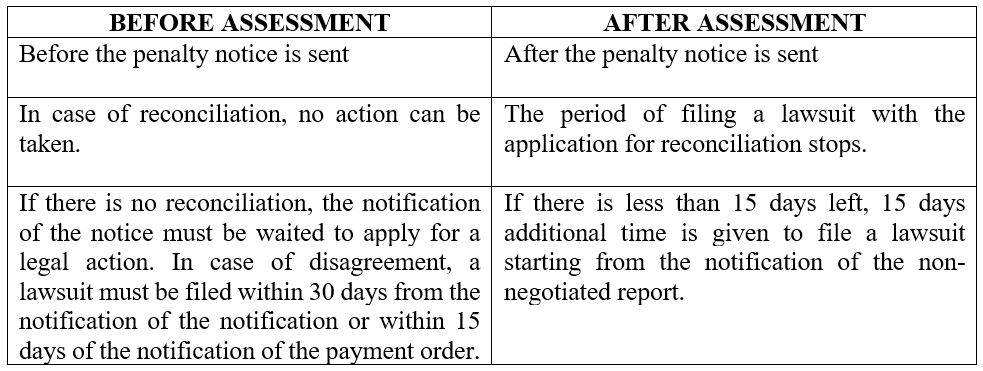

In pre-assessment settlement; Before the tax administration sends a notice after the tax inspection report, a reconciliation can be made.

If not, the taxpayer must file a lawsuit within 30 days after the tax penalty notice is sent to the taxpayer.

In the reconciliation after assessment, the application period stops during the evaluation of the application. If there is 15 days or less left or the period has expired, an additional 15 days is given to file a lawsuit after the settlement report has been drawn up.

Reconciliation blocks the way to file tax cases.

In the event that the taxpayers later learn that they are right, they cannot file a lawsuit against compromise.

Therefore, if we want to make a table before and after assessment;

The vast majority of the decisions made in the lawsuits filed against the notifications consist of “acceptance”, “rejection” or “partial acceptance / partial rejection”.

Taxpayers have the right to appeal or appeal against the decision if their case is rejected in whole or in part. However, appealing or appealing against the decisions taken in this way does not stop the execution of the action subject to the action. In order for the execution to be suspended, a decision for the stay of execution must be taken from the upper administrative judicial authority.